Home Mortgage Questions Answered In This Write-Up

Content written by-Kuhn McQueenIf you're looking into home mortgages, then you surely are excited. It's time to buy a home! However, what you might realize is there is quite a lot of information to take in, and how do you sort all of this out to get to the mortgage company and product that you need? Keep reading to find out how to do this.

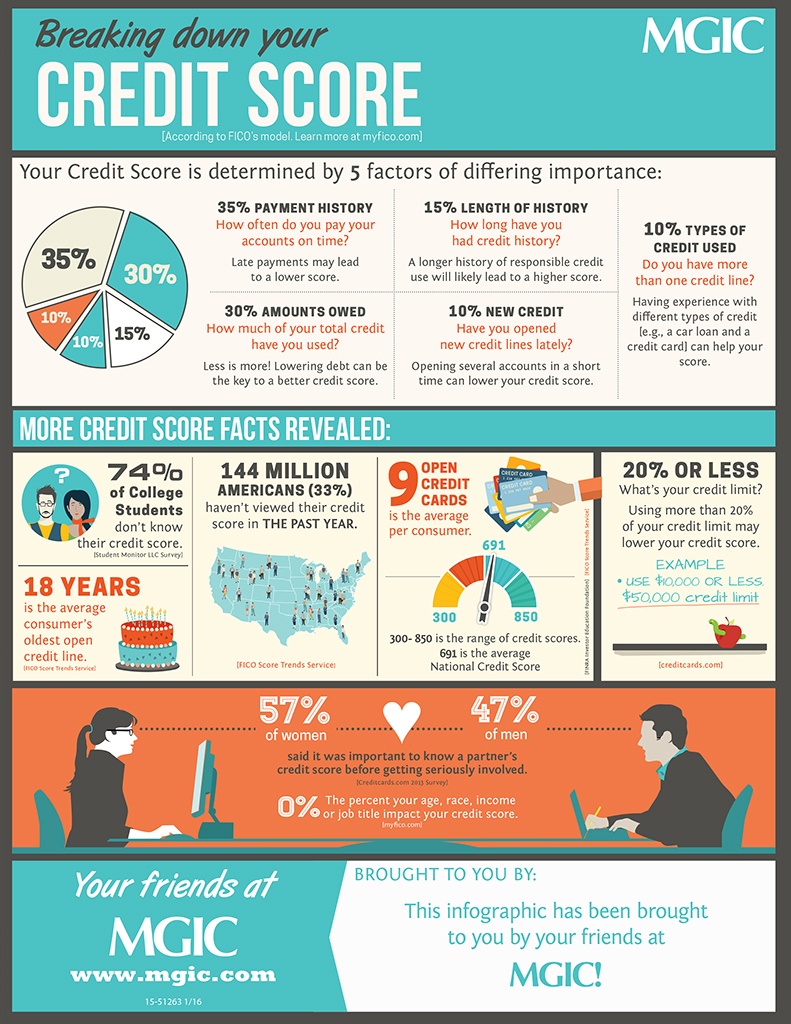

Check your credit report before applying for a mortgage. With today's identity theft problems, there is a slight chance that your identity may have been compromised. By pulling a credit report, you can ensure that all of the information is correct. If you notice items on the credit report that are incorrect, seek assistance from a credit bureau.

Your mortgage application might get denied in the final stages due to sudden changes to your overall financial standing. It's crucial that you are in a secure job position before getting a loan. Wait until after https://www.businesswire.com/news/home/20220215005111/en/Digital-Tools-Helping-Banks-Patch-Up-Relationships-with-Small-Businesses is approved to switch jobs if that's what you want to do.

When considering the cost of your mortgage, also think about property taxes and homeowners insurance costs. Sometimes lenders will factor property taxes and insurance payments into your loan calculations but often they do not. You don't want to be surprised when the tax office sends a bill and you learn the cost of required insurance.

Do not allow a denial from the first company stop you from seeking a mortgage with someone else. One denial isn't the end of the road. Continue to shop around and look at all of your options. You may need a co-signer to get it done, but there is a mortgage option out there for you.

Get quotes from many refinancing sources, before signing on the dotted line for a new mortgage. While rates are generally consistent, lenders are often open to negotiations, and you can get a better deal by going with one over another. Shop around and tell each of them what your best offer is, as one may top them all to get your business.

Never sign anything without talking to a lawyer first. The law does not fully protect you from the shrewd practices that many banks are willing to participate in. Having a lawyer on your side could save you thousands of dollars, and possibly your financial future. Be sure to get the right advice before proceeding.

Pay down your debt. You should minimize all other debts when you are pursuing financing on a home. Keep your credit in check, and pay off any credit cards you carry. This will help you to obtain financing more easily. The less debt you have, the more you will have to pay toward your mortgage.

Before looking to buy a house, make sure you get pre-approved for a mortgage. Getting pre-approved lets you know how much you can spend on a property before you start bidding. It also prevents you from falling in love with a property you can't afford. Also, many times seller will consider buyers with pre-approval letters more seriously than those without it.

Tell the truth. One lie and you could lose your mortgage. If a lender can't trust you to tell them the truth, then they likely won't want to lend you money.

Check out a minimum of three (and preferably five) lenders before you look at one specifically for your personal mortgage. Check with the Better Business Bureau, online reviews, and people you know who are familiar with the institution to learn of their reputation. Once you are familiar with each's details, you can make an informed decision as to which one is best suited for your personal situation.

Monitor interest rates before signing with a mortgage lender. If the interest rates have been dropping recently, it may be worth holding off with the mortgage loan for a few months to see if you get a better rate. Yes, it's a gamble, but it has the potential to save a lot of money over the life of the loan.

You must be demonstrably responsible to get a home mortgage. This means you have to have a good job that pays for your lifestyle with money to spare. Not only that, you must have been on the job for a couple of years or more, and you must be a good employee. The home mortgage company is entering into a long term relationship with you, and they want to know that you are ready to commit seriously!

Sellers know you are truly motivated to buy when you are prepared with a letter indicating you are approved for a home loan. It shows that you have already undergone a great deal of financial security and have received approval. The approval letter should be the amount of the offer you make. A high approval amount will show the seller that there is more you can pay.

You must be demonstrably responsible to get a home mortgage. This means you have to have a good job that pays for your lifestyle with money to spare. Not only that, you must have been on the job for a couple of years or more, and you must be a good employee. The home mortgage company is entering into a long term relationship with you, and they want to know that you are ready to commit seriously!

Give yourself time to get ready for a mortgage. Even in visit website of supposed instant Internet approvals, you need to take time preparing for a mortgage. This is time to clear your credit report, save money and maximize your score as much as possible. Give yourself at least six months in advance, although a year is better.

If you find incorrect information on your credit file, contact your credit bureau. There are so many instances of identity theft happening each year. For this reason, most credit bureaus have risk managers that have experience dealing with this type of thing. Also, the credit bureau can mark your credit report as one that has had their identity stolen.

Never quit a job while you are in the process of obtaining a home mortgage, even if the job is miserable for you. The lender may deny you because you are jobless. The lender may even pull out entirely, unsure of your future income.

During the process of obtaining a mortgage loan, submit any requested documents to your mortgage broker or lender as soon as possible. Taking your time to respond to your lender can delay the date of the closing. Delaying the closing date can put you at risk of losing the rate you have locked-in.

You must take the time to learn how to obtain the home loan that is right for you before applying for one. You want to find a home you can afford at the best rate possible for your situation. You don't want a home you can't afford. In the end, what you want is a home you can enjoy for years and a lender who is understanding and fair.